Life insurance cash value confuses a lot of people. An agent brings it up and suddenly the conversation shifts from “protecting your family” to something that sounds like a savings account inside your policy. Most people nod along and quietly wonder what they just agreed to.

This article explains exactly what cash value is, how it actually grows, what you can do with it, and when it genuinely makes financial sense for you.

What Is Life Insurance Cash Value

Life insurance cash value is a living benefit built into certain permanent life insurance policies. While you’re alive, a portion of each premium you pay accumulates inside the policy and grows over time. You can access that money through loans, withdrawals, or by surrendering the policy entirely.

This separates permanent life insurance from term life in a fundamental way. Term life is pure protection. You pay premiums, you get a death benefit if you die during the term, and nothing accumulates on the side. With cash value policies, there’s a financial component that grows alongside your coverage.

The cash value belongs to you while you’re living. The death benefit belongs to your beneficiaries after you’re gone. These two numbers are separate, and understanding that distinction upfront saves a lot of confusion later.

Which Life Insurance Policies Build Cash Value

Only permanent life insurance policies build cash value. Term life policies do not.

Here’s a clear comparison of the most common policy types:

| Policy Type | Builds Cash Value | Growth Mechanism | Risk Level |

|---|---|---|---|

| Term Life | No | N/A | None |

| Whole Life | Yes | Guaranteed fixed rate | Very Low |

| Universal Life | Yes | Current interest rates | Low to Moderate |

| Variable Life | Yes | Investment subaccounts | High |

| Indexed Universal Life | Yes | Market index with caps and floors | Moderate |

| Variable Universal Life | Yes | Investment subaccounts plus flexible premiums | High |

Whole life is the most straightforward. The growth rate is guaranteed by the insurer and does not fluctuate with the market. Variable life sits at the other end. Your cash value rises and falls with the investment options you select. Indexed universal life attempts a middle path by linking growth to a stock market index while offering a floor that protects against negative returns.

If you’re still weighing whether term or permanent coverage fits your situation better, this deeper look at term vs whole life insurance covers the practical trade-offs clearly.

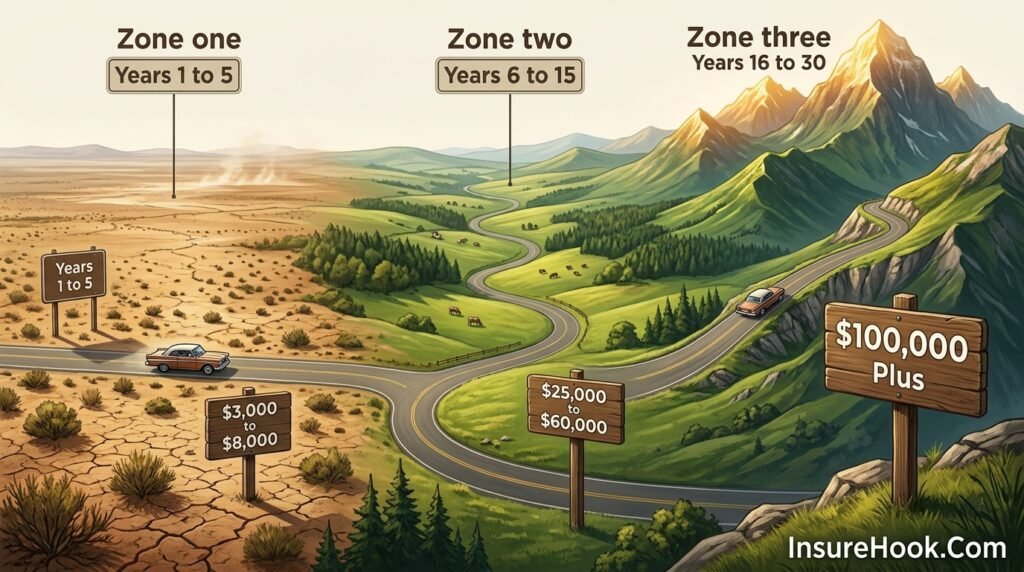

How Cash Value Actually Builds Over Time

Most people expect cash value to start growing immediately. It doesn’t work that way.

In the early years of a permanent policy, the bulk of your premium goes toward the insurance company’s costs and the pure cost of insurance. Only a small slice flows into your cash value account. Over time that ratio shifts. More of each premium feeds the cash value, and compounding starts to accelerate the growth.

Think of the first five years as the slow build. Years ten through twenty are where the momentum becomes visible.

Take Marcus, a 34-year-old who bought a whole life policy with a $500,000 death benefit. At year three his cash value was around $8,000. By year twelve it had grown past $60,000 without him doing anything beyond paying his monthly premium. He didn’t invest separately. He didn’t manage anything. The structure did the work over time.

This slow-start reality is exactly why people who cancel permanent policies in the first few years often walk away with less than they paid in. Surrender charges and front-loaded costs eat heavily into the balance during that window.

What You Can Do With Cash Value

Once your cash value reaches a meaningful balance, you have several real options.

Borrow Against Your Policy

A policy loan lets you borrow money using your cash value as collateral. No credit check. No income verification. No fixed repayment schedule. The IRS does not treat policy loans as taxable income as long as the policy stays in force.

The trade-off is real though. Interest accrues on the loan balance. If you let that interest compound without repaying anything, the loan can grow large enough to threaten the policy. If the outstanding loan exceeds your cash value, the policy lapses. At that point the IRS treats the entire gain as taxable income in a single year. That’s a painful outcome that’s entirely avoidable with basic monitoring.

If the insured person dies with an unpaid loan, the insurer subtracts the loan balance plus any accrued interest from the death benefit before paying beneficiaries. Your family still gets paid, just less.

Make a Partial Withdrawal

Some policies allow partial cash withdrawals. Amounts up to your cost basis (the total premiums you’ve paid) typically come out tax-free. Anything above that basis is taxable as ordinary income. Partial withdrawals also permanently reduce your death benefit. Unlike a loan, you cannot “repay” a withdrawal and restore what you took out.

Surrender the Policy Entirely

Surrendering means canceling the policy and walking away with the surrender value. That’s your current cash value minus any surrender charges the insurer applies. Surrender charges are common in the first ten to fifteen years and can be steep in the early years.

If you’ve held the policy long enough that your cash value exceeds your total premiums paid, you’ll owe ordinary income tax on the gain. You also lose all coverage permanently.

Use Cash Value to Pay Premiums

Once the cash value is substantial enough, many policies allow you to redirect it to cover your own premium payments. This feature provides flexibility during a financial hardship without requiring you to lapse or surrender the policy. The cash value decreases when used this way, so extended use can thin out the account.

The Tax Treatment of Cash Value

This is where a lot of people make costly assumptions.

Cash value grows on a tax-deferred basis. You don’t pay annual taxes on the gains as they build. This is a genuine advantage compared to a taxable brokerage account where dividends and capital gains get taxed each year.

The IRS has several specific rules about how life insurance cash value is taxed depending on what you do with it.

Policy loans: Generally not taxable while the policy remains in force. Taxable if the policy lapses or is surrendered with an outstanding loan that exceeded the cost basis.

Partial withdrawals: Tax-free up to your basis. Taxable above it.

Full surrender: Taxable on the gain above your total premiums paid.

Death benefit: Generally income-tax-free to beneficiaries under IRC Section 101(a), regardless of how much cash value had accumulated.

One important boundary worth knowing: the IRS uses a test called the Modified Endowment Contract (MEC) rule. If you overfund a policy too quickly (paying in more than the IRS limit allows), it gets reclassified as a MEC. Loans and withdrawals from a MEC are taxed differently and may carry an additional 10% penalty if you’re under age 59½. Avoid crossing that line.

The IRS publication on life insurance covers this in more detail if you want to go deeper on the tax rules.

Cash value life insurance gets oversold and undersold at the same time. Agents sometimes present it as an investment alternative, which sets unrealistic expectations. Others dismiss it entirely without considering what lifelong coverage and tax-deferred growth actually mean for the right client profile. The truth is context-dependent.

Cash Value vs. Death Benefit: A Common Misconception

Many people believe their family receives both the cash value and the death benefit when they die. Most standard whole life policies don’t work that way.

When you die, the insurance company pays your beneficiaries the stated death benefit. The accumulated cash value stays with the insurer. It essentially funded part of the company’s liability to you over the years. This is one of the most common points of confusion in permanent life insurance.

Some policies address this through paid-up additions riders or specific return of cash value features. Variable and universal life policies may structure the relationship differently. Always read the policy contract and ask your agent directly how the two numbers interact at death.

Understanding how your beneficiary receives a payout is just as important as understanding what grows during your lifetime.

Whole Life Cash Value: A Deeper Look at How Growth Works

Whole life deserves more detailed attention because it’s the most commonly sold permanent policy and the one that generates the most questions.

Your premium in a whole life policy is fixed for life. The insurer guarantees a minimum cash value growth rate embedded in the contract. In policies issued in recent years, that guaranteed rate has typically ranged from 2% to 4% annually, though this varies by insurer and issue date.

Many whole life policies from mutual insurance companies also pay annual dividends. Dividends are not guaranteed. They reflect the company’s actual financial performance including investment returns, mortality experience, and expense management. When declared, you can use dividends in several ways:

Take them as cash. Simple and flexible. You receive a check or deposit each year.

Apply them to premiums. Reduce or eliminate your out-of-pocket premium cost once the dividend is large enough.

Leave them in a dividend account. They earn modest interest inside the policy.

Purchase paid-up additions. This is the most powerful option for long-term growth. Each dividend purchases a small block of additional paid-up insurance, which itself has cash value and earns future dividends. Over decades, this compounding effect can significantly outpace the base guaranteed growth rate.

A woman named Carol bought a whole life policy at age 38 from a mutual company with a strong dividend track record. She chose to reinvest all dividends as paid-up additions. By her early 60s her cash value had grown well beyond what the guaranteed illustration projected, and her death benefit had increased meaningfully from the original face amount. She never touched the cash value but knew it was available if she needed it.

This kind of outcome is not guaranteed. Dividend scales change. But it illustrates why the type of insurer you choose matters when buying permanent life insurance.

The National Association of Insurance Commissioners maintains a consumer resource center that includes guidance on reading policy illustrations and understanding dividend projections.

When Cash Value Life Insurance Makes Sense

Cash value policies cost substantially more than term life. That’s not a hidden fact. A $500,000 whole life policy might cost four to eight times more in monthly premiums than the same death benefit in a 20-year term policy for the same person. The higher cost is only justified when the permanent features serve a real purpose.

Situations where cash value coverage genuinely fits:

People with a lifelong financial dependent, such as a child with a disability who will need support indefinitely. Term coverage would eventually expire. Permanent coverage doesn’t.

Business owners using permanent insurance for buy-sell agreement funding or key person coverage where the need doesn’t disappear after a set number of years.

High-income earners who have maxed out 401(k) and IRA contribution limits and want additional tax-deferred growth with more flexible access than retirement accounts provide.

Individuals focused on estate planning who want to pass wealth to heirs in an income-tax-free form.

Situations where term coverage is likely the better fit:

A parent in their 30s who needs $1,000,000 in income replacement coverage while children are young and a mortgage is outstanding. The need is real but time-limited. Buying a large term policy and investing the premium difference elsewhere often produces better long-term outcomes. This approach is sometimes called “buy term and invest the difference” and it’s a legitimate strategy for many households.

If you’re still figuring out how much coverage your situation actually requires, this guide on how much life insurance you need walks through the calculation practically.

Key Risks and Watch Points Before You Buy

Surrender Charges Can Trap You Early

Most permanent policies carry surrender charges that apply for ten to fifteen years. If your financial situation changes in year four and you need to cancel, you may receive considerably less than your total cash value. Always ask for a surrender charge schedule before signing.

Policy Illustrations Are Projections, Not Promises

When an agent shows you a policy illustration, the non-guaranteed column shows what could happen under current assumptions. For variable and indexed products, those projections can diverge significantly from actual results. Read both the guaranteed and non-guaranteed columns carefully.

Loans Compound Silently

Policy loan interest compounds whether you’re watching it or not. A loan taken out and ignored for years can grow into a serious problem. Set a reminder to review your loan balance annually at minimum.

State-Level Differences Matter

Insurance is regulated at the state level in the U.S. Policy terms, cash value protections, surrender charge limits, and consumer rights vary by state. The rules that apply to your policy depend on where it’s issued. Always verify your state’s specific regulations through your state insurance department or a licensed advisor in your state.

How Cash Value Fits Into a Broader Financial Plan

Cash value life insurance works best when it has a clear role in your financial picture rather than functioning as a standalone product sold on general appeal.

Financial planners who incorporate permanent life insurance typically do so after a client has established an emergency fund, is funding tax-advantaged retirement accounts, and has a specific reason why lifelong coverage is genuinely needed. It’s rarely the first financial tool to reach for.

If you already have a term policy and wonder whether converting it to permanent coverage makes sense as your needs evolve, understanding convertible term life insurance explains how that option works and what it costs.

Some people also carry multiple policies simultaneously, a term policy for heavy income-replacement coverage and a smaller permanent policy for lifelong needs. This layered approach can be cost-effective if structured thoughtfully. More detail on that strategy is available in this article on holding multiple life insurance policies.

Pre-Purchase Checklist for Cash Value Policies

Use this only if you’re actively evaluating a permanent policy. Skip it if you’re in early research mode.

Before signing a permanent life insurance application:

- Confirm that your need for coverage is genuinely lifelong and not just income replacement for a defined window of years

- Request the guaranteed column of the policy illustration and use it as your conservative baseline

- Ask for the full surrender charge schedule across years one through fifteen

- Understand the loan interest rate and whether it’s fixed or variable

- Find out whether the insurer is a mutual company (can pay dividends) or a stock company (typically does not)

- Ask explicitly how cash value and death benefit interact at death under this specific policy

- Confirm whether your state has specific consumer protections that apply to this type of policy

- Run the numbers against an equivalent term policy to understand the true cost difference

- Consult a fee-only financial advisor before committing if you’re unsure whether permanent coverage fits your financial goals

Free Estimator Tool

Cash Value Growth Estimator

See how cash value may grow over time based on your age, coverage amount, and monthly premium. Results are educational projections only.

FAQs

Whole life cash value carries a guaranteed floor. It cannot go negative. Variable life policies are different because the cash value is tied to investment subaccounts that can lose value if the market performs poorly.

In most standard whole life policies it does not. Your beneficiaries receive the death benefit. The insurer retains the cash value. Some policy structures and riders change this, so read your specific contract carefully.

Most whole life policies take seven to ten years before the cash value becomes large enough to use in any meaningful way. Accessing it before then often means paying surrender charges and receiving less than you put in.

Surrender value is cash value minus any applicable surrender charges. In the early years of a policy those charges can substantially reduce what you’d actually receive if you cancel.

Yes. Any unpaid loan balance plus accrued interest gets subtracted from the death benefit paid to your beneficiaries. The coverage stays active but the net payout decreases by the amount owed.

The policy lapses. At that point the IRS treats the total gain as taxable income in the year of lapse. This is why monitoring loan balances matters.

This article is for general informational purposes only. It does not constitute financial, tax, or legal advice. Life insurance products, regulations, tax treatment, and consumer protections vary by state and individual circumstance. Speak with a licensed insurance professional and a qualified tax or financial advisor before making any decisions about life insurance coverage.