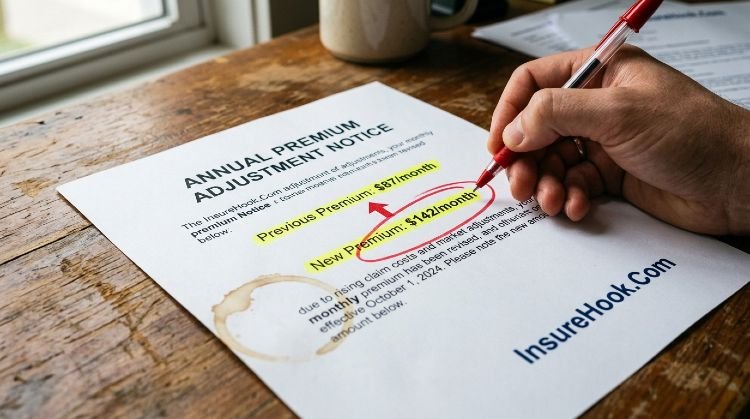

Sarah opened her life insurance renewal notice and froze. The premium jumped from $87 to $142 in one year. Her husband James checked his term life policy at the same time. His payment stayed exactly where it had been for three years. Why the difference?

The answer comes down to how their premiums were structured. Understanding fixed vs variable insurance premium helps you predict costs and avoid unwelcome surprises when bills arrive.

What Fixed Premiums Mean for Your Policy

A fixed premium stays the same for a specific period. You pay identical amounts each billing cycle. This structure appears most often in term life insurance and some disability policies.

The insurance company calculates your risk upfront. They lock in a rate based on your age and health at the time you apply. That number doesn’t budge for the duration of your contract term.

Many people find fixed premiums easier to budget. You know exactly what leaves your bank account each month. No guesswork. No recalculations.

Term life insurance policies typically offer fixed premiums for 10, 20, or 30 years. A healthy 35-year-old might pay $45 monthly for a 20-year term policy. That $45 stays put until the term ends.

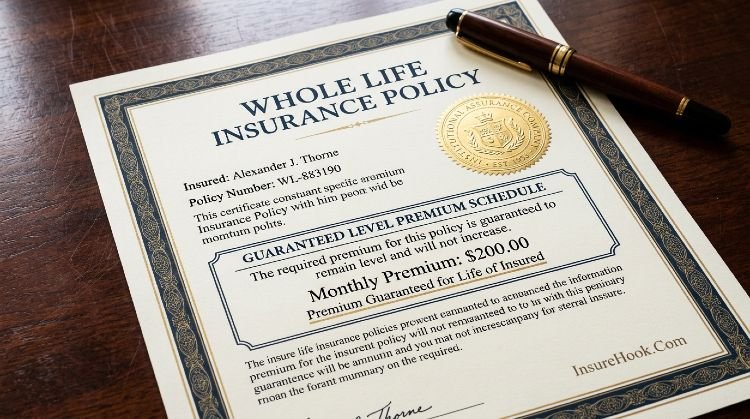

Some whole life policies also use fixed premiums. You pay the same amount from the day the policy starts until you die or surrender the policy. The predictability appeals to people who want stable financial planning.

How Variable Premiums Work

Variable premiums change over time. The amount you pay adjusts based on factors the insurance company reviews periodically.

Universal life insurance commonly uses this approach. Your premium might shift based on the policy’s cash value performance or changing mortality costs. These policies give you flexibility but remove payment certainty.

Auto insurance premiums can also vary. Your rate might drop after three years of clean driving. It could spike after an accident or moving violation. The insurance company reassesses your risk profile at each renewal.

Health insurance premiums change annually for most people. Insurers adjust rates based on age, location, and overall claims experience. A 40-year-old in Texas might see different increases than a 40-year-old in Oregon.

Term life insurance can have variable elements too. Some policies offer low introductory rates that increase every year or every five years. The initial savings look attractive but costs climb steadily.

Breaking Down the Cost Differences

| Feature | Fixed Premium | Variable Premium |

|---|---|---|

| Payment amount | Same each period | Changes over time |

| Budget planning | Simple and predictable | Requires flexibility |

| Common policy types | Level term life, whole life | Universal life, auto, health |

| Long-term cost | May be higher initially | Often starts lower |

| Risk to policyholder | Rate lock protects you | You absorb cost increases |

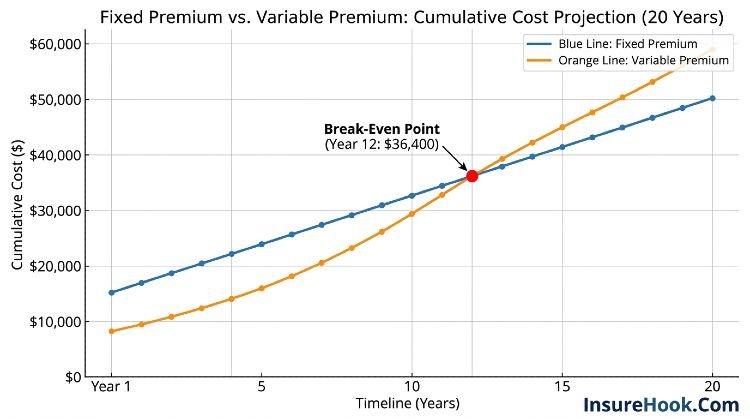

The tradeoff matters more than most people realize. Fixed premiums often cost more upfront because the insurer takes on the risk of future cost increases. They build a cushion into your rate.

Variable premiums might start cheaper. The insurance company can adjust later if their costs rise or your risk profile changes. You shoulder that uncertainty.

Why Your Premium Type Affects Your Budget

Michael bought a universal life policy at age 30. His initial premium was $65 monthly. The agent mentioned it could “adjust over time” but Michael focused on the low starting price. By age 45 his premium had climbed to $118. He struggled to maintain coverage during a tight financial year.

The premium type directly impacts how you plan your finances. Fixed rates let you set up automatic payments and forget about them. Variable rates demand periodic review of your budget.

Some families prefer knowing their insurance costs won’t change. Others accept variability in exchange for potential savings or policy flexibility. Neither choice is wrong. The right fit depends on your financial personality and situation.

Real Differences in Life Insurance Products

Term life insurance with fixed premiums dominates the market for good reason. A 30-year-old buys a 20-year term policy. She pays $42 monthly for $500,000 in coverage. That rate holds until she turns 50.

Universal life policies offer more complexity. The death benefit and premium can both flex. You might pay extra some months to build cash value. You might pay less when the cash value covers part of the insurance cost. This flexibility helps some policyholders but confuses others.

Whole life insurance locks in your premium forever. A $200 monthly payment at age 25 stays $200 at age 85. The insurance company takes considerable risk with this arrangement. They offset it by charging higher initial premiums than term policies.

Annual renewable term policies represent the most variable structure. Your premium increases every single year as you age. These policies start very cheap but become expensive quickly. Few people keep them past age 50.

What Drives Premium Changes in Variable Policies

Insurance companies don’t change variable premiums randomly. Specific factors trigger adjustments.

Your age matters most. Older policyholders cost more to insure. Universal life policies often increase premiums as you move into higher age brackets.

Cash value performance affects some policies. If your policy’s investments underperform, you might need to pay higher premiums to maintain the same death benefit. Strong performance could lower your required payment.

Broader claims experience influences rates too. If an insurance company pays more claims than expected across their entire book of business, they might raise premiums for everyone with variable-rate policies.

Some health insurance policies adjust based on your specific claims. File expensive claims and your next renewal might bring a rate increase. Go years without claims and some insurers reward you with lower premiums.

State regulations limit how much and how often insurers can change certain premiums. These rules vary widely depending on where you live and what type of insurance you carry. The National Association of Insurance Commissioners provides state-specific regulatory guidance that affects how premiums work in your area.

Evaluating Which Premium Type Fits Your Needs

Think about your income stability first. Does your paycheck vary month to month? Fixed premiums might provide welcome consistency. Steady income with room for adjustment? Variable premiums become less risky.

Consider your financial planning style. Some people build detailed budgets years in advance. They want every expense nailed down. Fixed premiums suit this approach perfectly.

Others prefer adapting as life changes. They don’t mind reviewing and adjusting their insurance costs periodically. Variable premiums work fine for this group.

Your age and health also matter. Young healthy buyers often get excellent fixed rates. Locking in a low premium for decades makes sense. Older applicants or those with health issues might face high fixed rates. Variable options could start more affordably.

The policy duration plays a role too. Need coverage for a specific period? Fixed-rate term insurance makes sense. Want lifelong coverage with flexibility? Variable options might fit better.

Common Misconceptions About Premium Structures

Many people assume variable premiums always cost less overall. That’s not guaranteed. Some variable policies end up more expensive than fixed alternatives when you total all payments.

Others think fixed premiums never change. That’s mostly true during the level premium period. But when a term policy renews after 20 years, the new fixed rate usually jumps dramatically. You’re 20 years older and much more expensive to insure.

Some buyers believe insurance companies can’t touch fixed premiums. State regulations actually allow premium increases under certain circumstances even for fixed-rate policies. These situations are rare but possible.

The idea that variable premiums give you more control sounds appealing. In reality, you rarely control when or how much the premium changes. The insurance company makes those decisions based on their formulas and state-approved rating structures.

How State Laws Affect Your Premium Options

Insurance regulation happens at the state level. This creates real differences in how premiums work depending on where you live.

California restricts auto insurance rating factors more than many states. That affects how variable your car insurance premiums can be. Texas allows more rating flexibility. Your premium might fluctuate more there.

Some states require guaranteed renewable health insurance. The insurer must offer renewal but can adjust the premium. Other states add restrictions on how much rates can increase year to year.

Life insurance faces less state variation in premium structures. But state guarantee associations and reserve requirements still influence what insurers offer in different markets.

Looking at how premium types compare helps clarify your options within your specific state’s rules.

Questions to Ask Before Choosing a Policy

What happens to my premium at renewal? This matters especially for term life insurance. Some policies guarantee the renewal rate. Others leave it open-ended.

Can the insurance company raise my fixed premium? Get this answer in writing. Most truly fixed premiums stay locked. But understanding exceptions protects you.

What factors trigger variable premium changes? You deserve specifics. Age-based increases? Investment performance? Claims experience? Know what you’re signing up for.

Does the policy include rate guarantees or caps? Some variable policies limit annual increases. Others promise rates won’t exceed certain amounts. These protections matter.

How does the premium compare to similar policies? Shop around before committing. Fixed and variable options from different insurers can vary dramatically in cost and terms.

Reading Your Policy Documents Carefully

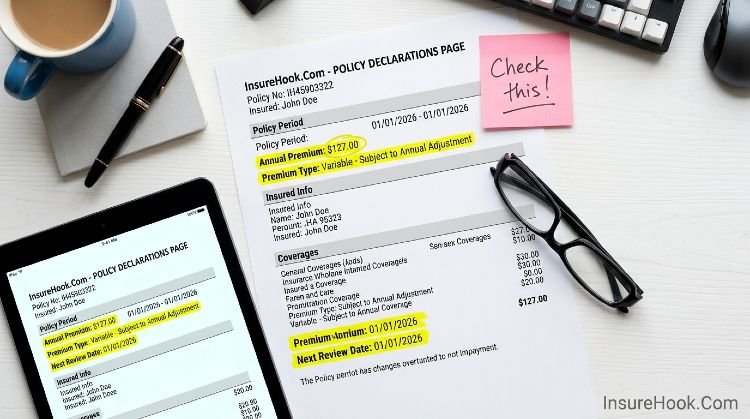

Your insurance declarations page shows your current premium and type. Check whether it lists a guaranteed level term or indicates potential adjustments.

The policy contract explains premium change conditions. This section usually appears in dense legal language. Read it anyway. Look for phrases like “subject to adjustment” or “guaranteed level premium.”

Some policies include premium schedules. These charts show exactly what you’ll pay each year or each age bracket. This information removes guesswork from budgeting.

Annual notices often explain premium changes. Don’t toss these letters unopened. They tell you what you’ll pay next period and sometimes explain why the amount changed.

Understanding how to read your insurance policy prevents surprises and helps you verify you got the premium structure you expected.

When Fixed Premiums Make the Most Sense

You want absolute budget certainty. Fixed premiums deliver exactly that for their guaranteed period.

You’re young and healthy enough to lock in favorable rates. A 30-year-old non-smoker can secure incredibly low fixed premiums on term life insurance. Waiting until 40 or 50 means higher locked-in rates.

You need coverage for a specific time period. Paying off a 20-year mortgage? A 20-year fixed-rate term policy matches perfectly.

You prefer simple insurance products. Fixed premiums usually come with straightforward policies. Less flexibility means fewer moving parts to track.

You plan to keep the coverage long-term. Locking in today’s rate protects you from future increases due to age or health changes.

When Variable Premiums Might Work Better

You want the lowest possible starting premium. Variable policies often beat fixed options on initial cost.

You like flexibility in death benefits and payments. Universal life policies let you adjust coverage and premiums as your needs change.

You’re comfortable with some financial uncertainty. Variable premiums require accepting that your costs might rise.

You expect your income to grow significantly. Starting with lower variable premiums becomes easier to absorb as you earn more.

You want cash value features with your life insurance. Most cash value policies use variable premium structures to accommodate policy complexity.

The Role of Premium Structure in Long-Term Planning

Insurance fits into broader financial goals. The premium structure affects how well it integrates with your plan.

Fixed premiums work beautifully in detailed retirement projections. You know exactly what you’ll spend on insurance each year. That certainty helps with income planning.

Variable premiums require building in assumptions and cushions. You might budget for 5% annual increases and hope the actual changes stay lower.

Estate planning often relies on permanent life insurance. These policies typically use fixed premiums. Knowing the exact cost until death helps trustees and beneficiaries understand the estate’s cash flow.

Business insurance for buy-sell agreements usually works best with fixed premiums. Partners want predictable costs in their operating budgets.

Disability insurance commonly offers both options. Many professionals choose fixed premiums to guarantee their coverage stays affordable even if their health changes.

What Happens When You Can’t Afford Premium Increases

Variable premiums that climb beyond your budget create tough choices. You might reduce your death benefit to lower the premium. This keeps some coverage in place but leaves your family with less protection.

Some policies let you convert to paid-up insurance. You stop paying premiums and accept a smaller permanent death benefit. This option beats losing coverage completely.

Taking a grace period gives you time to catch up on payments. But this only delays the problem if you genuinely can’t afford the new premium level.

Shopping for new coverage might make sense. You could find a fixed-rate policy that costs less than your increasing variable premium. Your age and health at the new application will determine if this works.

Letting the policy lapse loses all coverage and potentially all cash value. Understanding policy lapse consequences helps you avoid this outcome.

Expert Perspective on Premium Choices

A certified financial planner with two decades of experience notes a clear pattern. “The premium structure should match your financial personality more than anything else. I’ve seen people stress over $10 monthly fluctuations in their car insurance. Those individuals need fixed premiums on their life insurance. Others barely glance at their bills. They handle variability just fine.”

That guidance rings true across thousands of insurance decisions. Your comfort with uncertainty matters more than theoretical savings.

Some financial advisors push variable premium products because they offer higher commissions or more features to discuss. Good advisors match the product to your actual needs and preferences.

The insurance industry slowly shifted toward more fixed-rate products in life insurance. Consumers demanded simplicity and predictability. Universal life policies grew popular in the 1980s but term insurance now dominates new sales.

Auto and home insurance remain largely variable by nature. Your risk profile genuinely changes year to year. Insurers need flexibility to price that accurately.

Health insurance became almost entirely variable due to rising medical costs. Fixed health premiums would require such high rates that few people could afford coverage.

Making Your Decision

Start by listing what matters most in your insurance coverage. Stable costs? Maximum flexibility? Lowest initial price? Longest guarantee period?

Get quotes for both fixed and variable options. Compare the initial premiums and projected long-term costs. Some insurers provide illustrations showing potential premium paths.

Read the fine print on what triggers premium changes. Make sure you understand and accept those terms before buying.

Consider working with an independent agent who represents multiple companies. They can show you various premium structures without pushing a single product.

Trust your instinct about budget comfort. If premium uncertainty will keep you up at night, pay extra for a fixed rate.

Peace of mind has real value.

Fixed vs Variable Premium Calculator

See how a fixed premium compares to variable market-linked costs over your policy term.

Your 10-Year Cost Comparison

This tool is for educational illustration only. Actual variable premiums depend on your specific policy, insurer, and market conditions. Consult a licensed insurance professional before making coverage decisions. Insurance rules vary by state.

Frequently Asked Questions

True fixed premiums stay level during the guaranteed period. After a 20-year term ends, renewal rates jump significantly. Some policies also allow increases if you make material misrepresentations on your application. But for the stated level period, properly structured fixed premiums don’t change.

Variable premiums can move in either direction. Strong cash value performance might lower your required payment in universal life policies. Improved health or better driving records could reduce auto insurance premiums. Age and rising costs push rates up more often than other factors push them down.

It depends entirely on the specific policies and how long you keep them. Fixed premiums often total less for term life insurance held to full term. Variable premiums sometimes win for shorter holding periods or if you die earlier than expected. Universal life policies vary so much that generalization becomes impossible.

Most policies don’t allow premium structure changes without replacing the entire policy. Some universal life contracts let you lock in premium levels by reducing flexibility. You’d need to apply for a new policy to truly switch structures. That means new underwriting based on your current age and health.

Check your policy declarations page and contract. Look for terms like “level premium” or “guaranteed premium” or “subject to adjustment.” Your insurance company or agent can clarify. Annual statements often indicate if your next premium will differ from your current payment.

The insurer builds projections and cushions into fixed premiums. They estimate future costs and charge accordingly. They might make less profit than expected if costs exceed projections. But they rarely lose money. Careful actuarial work and diversified risk pools protect them.

This article provides general educational information about insurance premium structures in the United States. Insurance products and regulations vary significantly by state, insurer and individual circumstances. This content does not constitute financial or legal advice. Consult with licensed insurance professionals and review all policy documents before making coverage decisions.