Have you ever used an insurance claim? It may be quite a stressful period. Perhaps there was an accident to your car. Or your house was a casualty of the storm. You simply desire things to be right. Here is where one important word is used. Most insurance exists on its basis. Indemnity we are speaking of.

What then is indemnity in insurance? Indemnity is nothing more than a mere promise. It is an assurance on the part of your insurer. They assure you that they will make you financially whole. They will take you back to where you have been. Financial status immediately before the loss.

This is a very significant argument. It is not to make a profit on your part. Insurances are concerned with recovery and security. It does not happen to win the lottery. Learning this concept will make you know what to expect. It allows you to manoeuvre your policy in real confidence.

The awareness of indemnity guarantees a reasonable payout. This principle impacts on all aspects of your policy. It affects your payment of premiums. It also affects your end of claim check. Now let us enter deep into this important principle of insurance. We are going to discuss precisely what is meant by indemnity.

The Ultimate Principle of Indemnity Illustrated.

Insurance is supported by the principle of indemnity. This is an essential legal principle. It has an objective that is simple and just. It makes it impossible to make any profit by any policyholder. An insured loss is not money making. Insurance is a protectionist.

Consider that you are robbed of your old television. It was about ten years old. The doctrine of indemnity works here. You earn money on a ten-year-old television. Not even to a brand new, top-of-the-line screen. This system assists in making insurance affordable to everybody.

Moral hazard is also avoided by this rule. It prevents human beings intent to make losses. The insurance system cannot be without it. The entire industry is based on this equitable concept. It makes sure that the system is not volatile.

The Key Objective: Rebuilding Your Financing State.

The overarching concept is that of restoration. We desire to put you there where you began. You should be no better off. And you should be no worse off. Consider it as a money clean button to you. You lose, and you have reset your insurance.

This will restore the financial position to the pre-loss position. It is an effective monetary insurance. This is applicable to most types of losses. The car accident is a very easy example. Your insurance company covers the cost of fixing your car. Or they bring you its cash equivalent.

This will compensate your loss of money. It will not leave you with a brand new luxurious automobile. It solely attempts to heal you back to whole. This is what the promise of indemnity is all about.

The Importance of the Principle of Indemnity to You.

This principle has a direct effect on your wallet. It acts to make your insurance premiums reasonable. Rates would skyrocket in case individuals were able to make an easy buck out of claims. Everybody would have a rationale to make a loss. The maintenance of the system would be too costly.

This is a large cause of concern over the effect of inflation on the increasing cost of insurance. It just complicates the process of restoration by making insurers have to spend more money. Their increased prices translate to increased premiums to you.

Basic honesty is also encouraged in indemnity. It acts as a formidable deterring factor to fraudulent claims. The task of the insurer is to indemnify you. That is, they will make you a loss proven by you. This is a just system that puts us all in the right positions. It builds essential trust.

Insurance lies in the foundation of indemnity. It makes sure that the aim of insurance, which is to restore a person to wholeness, is achieved without providing a chance to make a profit. – Insurance Industry Analyst

The Secrets of Insurance Companies on Payout Calculation.

When you make a claim a process is initiated. The insurance adjuster has to arrive at a value. And they require the worth of your loss of money. They do this calculation in some particular ways. These approaches are premised on the concept of indemnity.

There are two primary methods that are quite widespread. Those are the Actual Cash Value and Replacement Cost. It is essential to you to know them. It is this kind of understanding that will dictate the amount of money you receive. Depending on what method is applicable is stipulated in your policy documents. We can divide their meaning.

Actual Cash Value (ACV)

A very common method is the Actual Cash Value (ACV). Most insurance policies are defaulting. ACV covers the cost of a replacement of an item. However, which is important, it deducts depreciation. Depreciation refers to the value loss with the lapse of time.

This value depreciation occurs because of age. It is also caused due to wear and tear. Let’s use a clear example. Your five year old sofa burns down. You would spend another $1,000 on a new similar sofa. But your old sofa was worn out some.

The adjuster may indicate that it has depreciated by 40 per cent. Then it has the real cash value of $600. It is 600 dollars that the insurance company is going to pay. You would be required to pay an additional 400 to get a new one.

Chart: ACV on a Simple Calculation.

The following grid is an illustration of the ACV in the case of a laptop. This renders the math easy to grasp.

Insurehook — Laptop Depreciation & ACV

Depreciation vs Remaining Value (After 3 years)

Cost / Depreciation / Payout Comparison

Value Over Time (5-year lifespan, 20% p.a. straight-line)

Replacement Cost Value (RCV)

Replacement Cost Value (RCV) is rather different. It tends to be a more liberal form of coverage. RCV makes no deduction on any depreciation. It covers the entire price to replace your product. This comes with a new, similar item.

Such coverage is normally expensive. RCV policy premiums are increased. However, the dividend is more attractive to you. It gives one more peace of mind. You may very well substitute just what you lost. This will assist you to get back on your feet in a lot shorter time.

Using our sofa example again. RCV policy would provide you with 1k. This is the entire price of a new similar sofa. This coverage is favored by a number of homeowners and renters. It bridges the difference between depreciation.

A Rapid Comparison of ACV and RCV.

| Feature | Actual Cash Value (ACV) | Replacement Cost Value (RCV) |

|---|---|---|

| Payout Basis | Cost to replace minus depreciation. | Cost to replace with a new, similar item. |

| Premium Cost | Lower | Higher |

| Out-of-Pocket Expense | You pay the difference (depreciation). | Little to no out-of-pocket for the item. |

| Best For | Budget-conscious individuals. | Those wanting maximum protection. |

Indemnity Across Various Insurance Policies

The principle of indemnity is not a universal principle. Its usage varies between insurances. The same can not be said of your car. It is not similar to the way it works regarding your health. However, the centralized thought is always the same.

Your aim is always to make up your financial loss. The technique only varies to suit the scenario. Let us look at some of the popular insurance examples. This will make you feel indemnity at work.

Home and Renters Property Insurance.

It is the purest application of indemnity. There is a price on your house and your possessions. In case they are broken or stolen, then you lose. Property insurance is meant to cover your loss. Taking an example of planning a big move, the act of insuring your belongings is pure indemnity.

Your kitchen could be burnt down in a fire. To rebuild it, your policy will be paid. The coverage varies depending on your coverage. It could be ACV or RCV. Geographical location may also be a causative factor. Problems such as Florida home insurance rate caps indicate the influence of external factors on the value and payouts of policies.

Auto Insurance

Another day-to-day occurrence of indemnity is auto insurance. In the case of an accident, your policy will come in and repair your car. It even puts your vehicle back to its state before the accident. When added up you obtain the actual cash value.

Indemnity is also a liability coverage. It compensates on the other individual damages. This is to keep in mind in case you are planning to change auto insurance. You wish to make sure that your new policy has good indemnity covers.

Health Insurance

Health cover is an exception of indemnity. Your health really cannot attached with a price tag. It is another type of indemnity, then. The policy protects you against the cost of high medical expenses. It pays hospital expenses and physician visits.

This coverage will save you a crippling medical debt. You are always partial to the expense, of course. Such policies are necessary in certain states. This can observed in locations where there are certain updates of the health insurance mandates. And when travelling worldwide, a travel medical insurance guide would be crucial in keeping safe.

Liability Insurance

Liability insurance is pure indemnity cover. It covers your financial loss on lawsuits. This may include a home or auto policy. Or it may be an independent umbrella policy. In case of an accident to somebody on your property they might also sue.

Their medical bills are paid by your liability insurance. It is also inclusive of your defense costs. It makes any payment or judgment against you. This will be within your certain policy limits. It compensates the injured individual on his or her loss.

Major Concepts that are related to the Principle of Indemnity.

There are a number of additional insurance terms that are closely related. They are connected to the indemnity principle. They are all collaborative in order to be fair. Also they do not allow you to receive two losses out of the same loss. They also determine what you are covered with.

That is the reason why the principle of indemnity works in the real world, according to the checks and balances offered by the concepts of subrogation, insurable interest, and policy limits. – Insurance Law Legal Scholar.

Subrogation: The Right to Recover.

Subrogation is a cumbersome term that has a plain task. Suppose a car is struck by another driver. The repair of your car is insured. They do not take long to ensure that you are not waiting. You are now made whole again.

Thereafter, your insurer can take up your shoes. The at-fault driver can pursued by them legally. They will make claims against the insurer of that driver. This process is subrogation. It makes you not pay twice on the loss.

You and the Deductibles and the Loss.

The amount that you pay out is your deductible. It is your portion of the risk as you have agreed. In case you have a deductible of $500, you can pay that first. You cover the initial payment of 500 dollars of repair bill. The remaining part is then paid by your insurance company. This is a form of co-indemnity.

Deductibles enable you to maintain low premiums. They also do not encourage very small and frequent claims. Assuming a minor portion of the risk, you contribute to the entire system. It demonstrates that you have skin in the game.

Policy Limitations and Exclusions.

Every policy has its limits. This is what the insurer will pay by the most. Maximum that you can get 300,000 dollars of the house that you live in is insured. This is one of the significant elements of the indemnity contract. You are only indemnified to limit you mentioned.

There are also exclusions of the policies. These are certain things that the policy will not encompass. It is important to comprehend what an exclusion in a policy is critical. It informs you of precisely where the coverage limit and your individual financial liability line, or limit.

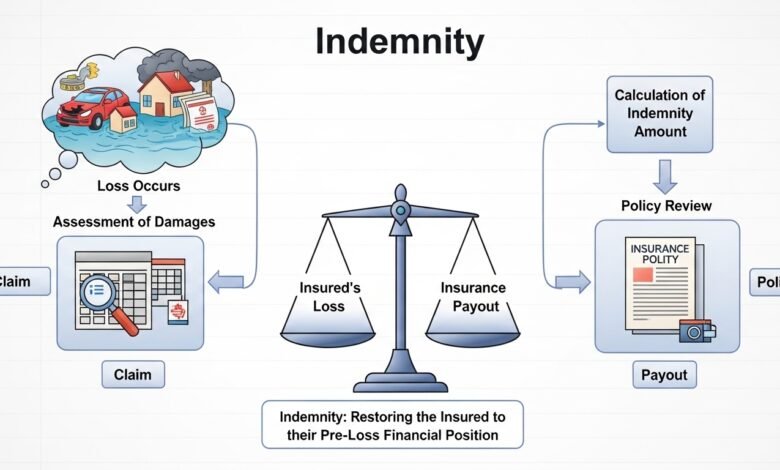

The Indemnity Claim Process — Zig-Zag

Loss Occurs

Example: A tree falls on your car.

You File a Claim

You contact your insurance company to report the loss.

Insurer Investigates

An adjuster assesses the damage and reviews your policy.

Value is Calculated

Using ACV or RCV, minus your deductible.

Indemnity is Paid

You receive a check for the covered amount.

Subrogation

If applicable, your insurer seeks payment from the at-fault party.

Exceptions to the Rule of Indemnity

Although indemnity is a fundamental rule, there are policies that operate in a different manner. These are normally policies where a loss cannot be easily valued. They can made to give a fixed amount of money. This provides another type of financial security.

Life Insurance

The largest exception is life insurance. It does not indemnify as such. A human life cannot given a financial value. Rather it will referred to as a valued policy. It makes an agreed amount of money. This is the death benefit.

This amount is received by the beneficiary. This finances assist them in managing the financial blowback. It will be able to cover lost earnings or settle debts. The issue of determining the appropriate amount is important. The same applies regardless of whether you are considering life insurance maxing at various ages.

Valued Policies

Valued property insurance policies are some of them. This applies to unusual and valuable products. Consider traditional automobiles or art masterpiece. Or some precious jewelry and collectibles. Their real cash value is difficult to establish.

Therefore, you and the insurer come to a value at the beginning. This agreed value is inculcated in the policy. In case the item is lost, the insurer compensates the amount. Arguments regarding depreciation are nonexistent. This is clarified by state laws which are explained in an outside source such as the Insurance Information Institute.

Future of indemnity and insurance technology.

The world of insurance never stays the same. The process of indemnity is being expedited by technology. It is also rendering it more accurate. It is also more customer-friendly than ever. Such innovations are transforming the entire industry.

The first line of attack has taken by new and exciting insurtech startups. They apply AI and big data in order to make everything streamlined. Take into consideration the new telematics insurance devices that are available.

These devices have the ability to monitor your driving patterns. Good drivers are able to achieve a lot less premium. This is a contemporary variation of risk sharing.

Solution: Your Partner in Financial Recovery.

What is indemnity in insurance then? It is a guarantee of total rebuilding. The main pillar that ensures that insurance functions is it. It guarantees that you will be complete following a loss. It is of bringing you back on your feet.

Even in your car, even to your house, indemnity. It cushions you against economic calamity. You are a smarter consumer by having known such terms as ACV and RCV. Then can be able to select the appropriate policies. You will be able to maneuver claims with all the confidence.

Insurance shares with you in dealing with the risks of life. And the rulebook is the principle of indemnity. It maintains a partnership that is just to all. This is one of the fundamental concepts that you should remember as you go on with your journey of insurance. It is the secret to your future prosperity, the real meaning of the word indemnity.

Frequently Asked Questions (FAQs)

The word indemnity refers to putting you back to the same financial status that you had immediately before a loss. It is not about having you make a profit when you can have you made whole again.

ACV compensates you regarding the value of an item, but not the depreciation. RCV covers the complete price to substitute the product with a new one which is similar but not deduced by loss of value.

No, this is not the case with life insurance. It is a “valued policy.” It pays a set sum of money because you cannot give a financial estimation of the worth of a human life.

Subrogation occurs when your insurer, once he or she pays your claim, attempts to collect money against the party at fault. This facilitates indemnity as it ensures that you are not remunerated twice.

The deductibles are your part of a loss. They assist in making premiums affordable. They also do not favor filing the small claims, and you are a partner in the risk management.

![Does Renters Insurance Cover Bike Theft Outside Home? [2026 Expert Guide]](https://insurehook.com/wp-content/uploads/2026/01/11-8-390x220.jpeg)